Pre-Revenue Cross-Border Tax Planning (R&D Cost Recharge Arrangement) needed

Hong Kong has been promoting itself as the Asian R&D hub in recent years. Lots of subsidies have been provided by the HKSAR government, HKSTP (Science Park), Cyberport and other organisations to encourage MNCs to set up their R&D center in Hong Kong. Meanwhile, as Hong Kong is just a small city with small population size, very often these MNCs would carry out R&D activities in other tax jurisdictions as well (e.g., the PRC, the US, Taiwan).

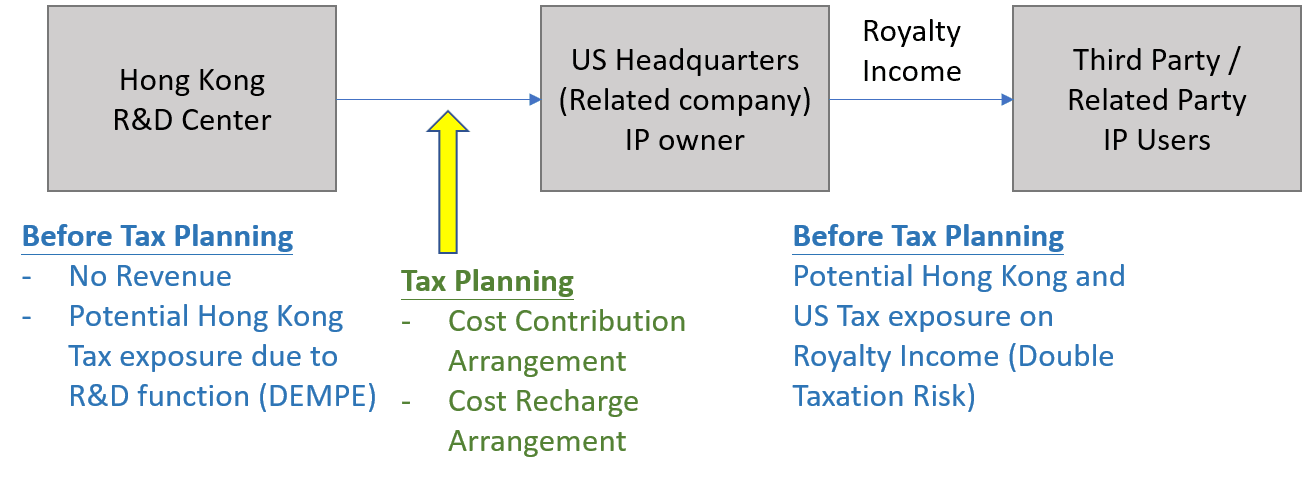

Effective from the year of assessment 2020/21, Section 15F of the Inland Revenue Ordinance (IRO) has been proven to be a catalyst for taxpayers with R&D functions in multiple locations (including Hong Kong) to implement tax planning. In particular, it applies to the following situations:-

A Hong Kong company has been set up to carry on R&D functions in Hong Kong. Most of them are located in Science Park, Cyberport and other incubation centres;

The legal title of the Intellectual Property (IP) generated from the R&D activities does not belong to the Hong Kong company despite the fact that the Hong Kong company contributes all or part of the value creation processes (i.e., DEMPE [1] );

Particular attention would be paid by the Inland Revenue Department (IRD) if the IP legal owner is located in low-tax jurisdictions (e.g., the BVI, Cayman Islands); and

The IP is expected to generate income in the future either via licensing (royalty) income or sales of IP.

Section 15F of the IRO allows the IRD to impose Hong Kong Profits Tax on the income generated from the IP even though the legal owner of the IP is a non-Hong Kong tax resident as long as part or all of the R&D activities are performed in Hong Kong. In most cases, the overseas legal owner is a related company of the Hong Kong company.

The underlying principle is that taxpayers should pay tax in their value creation jurisdiction / operating jurisdiction (i.e., Hong Kong in this case) over the place of incorporation of the legal owner.

Double Taxation risk arises as the legal owners of the IP may also have to pay tax in their own jurisdictions. If that jurisdiction is not a Double Taxation Agreement (DTA) partner of Hong Kong (e.g., the US and Taiwan), tax credit may not be available to resolve the double taxation risk.

[1] Development, Enhancement, Maintenance, Protection or Exploitation