Deductibility of Keyman Insurance Policy

Keyman insurance policy may not be a good means for the tax planning of SME businesses

It is common for a company to insure against the loss of profits arising from the death, sickness or injury of a key employee. The beneficiary of the insurance policy is usually the employer. It is known as the keyman insurance policy.

It is worth to note that the insurance premiums paid are not always deductible. The Inland Revenue Department (IRD) has listed out some conditions in its Frequently Asked Questions.

The premiums paid are only deductible if:

In the case of a life insurance policy, it is a term insurance, covering the life of the employee within the term of the policy, with no other benefits;

The purpose of taking out the insurance is to compensate the employer for the loss of trading income that may result from the loss of the service of the key employee in case of death, sickness or injury.

In contrast, the IRD has illustrated some scenarios that the premiums paid are NOT deductible:

CENARIO | REASON |

|---|---|

The insured person is a sole proprietor or a partner | It is not an employer and employee relationship under a sole proprietorship or partnership |

The insured person is a director of a limited company who owns not less than 20% of the company’s share | The premiums paid are of capital in nature since the purpose of the policy is to protect the value of shares |

The proceeds are payable to the family member of the employee | The policy is not to compensate the employer’s loss of profits |

The policy is an investment-linked policy | The premiums for the investment portion are not deductible because they are of a capital nature. Only the premiums for the risk portion are deductible. |

POINTS TO NOTE

For many family businesses in Hong Kong, the owners are both the 100% shareholders and directors of the company at the same time. They always aim to find ways to reduce the overall tax payable of the company and themselves. Based on the above analysis, keyman insurance policy obviously cannot fulfill their purposes.

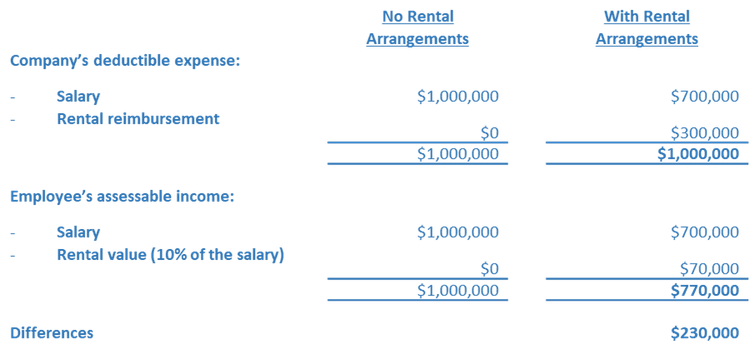

Similarly, dividend and salary arrangements would not help much as well. Rental Reimbursement / Rental Value Arrangements (detailed calculation at the end) and Staff Medical Card Arrangements may help but there is a limit on the amount of benefits.

For detailed requirements of Rental Arrangement, please refer to our November 2021 Newsletter.

A common wrongdoing committed by the taxpayer would be the settlement of directors’ personal expenses by the corporation. The corporation would claim tax deduction on these expenses while the director would not report such amount as employment income.

They may not notice that this is an incorrect tax treatment or they may have a misconception that the worst consequence would be disallowance of expense tax deduction only. Some of them may have even made up fictitious expenses to try to reduce the profits and tax payable.

In reality, many SME taxpayers are now facing Field Audit and Investigation of the IRD these two years. Not only their private expenses would be disallowed, but also they would be subject to maximum penalty in the amount of three times of tax undercharged and imprisonment as well. They also suffer from a painful investigation process, including attending interviews with the IRD.

Rental Value Calculation:

For the detailed conditions and implementation of the housing benefit and other tax planning, it is always advisable for you to contact your tax consultant.