文章

Carried Interest Tax Concessions For Fund Managers – Introduction to Tax Relief on Hong Kong’s Limited Partnership Funds and Open-Ended Fund Companies (英文版本)

暂时只提供英文版本

Henry Kwong, Tax Partner, Cheng & Cheng Taxation Services Ltd, analyses the latest guidance from Hong Kong’s Inland Revenue Department (IRD) on the unified funds tax exemption regime and carried interest tax concessions.

With the aim of upholding Hong Kong’s position as ‘a premier international asset and wealth management centre’ in the face of fiercer competition, the HKSAR Government introduced a limited partnership fund (LPF) regime and relaxed the requirements for open-ended fund companies (OFCs). To support the development of the fund industry, the government has also introduced a tax exemption regime for funds, as well as tax concessions on carried interest (performance fee). Together with the proposed tax concession for family offices, these tax incentives will provide tremendous support to Hong Kong fund managers and will attract global asset managers to relocate their Asian centres to Hong Kong.

The Inland Revenue (Profits Tax Exemption for Funds) (Amendment) Ordinance 2019, which came into effect on 1 April 2019, seeks to exempt most type of funds from Hong Kong profits tax. The unified funds exemption (UFE) regime provides a unified tax treatment for all funds operating in Hong Kong. In addition, investment managers of private equity funds can enjoy a 0% tax rate on qualified carried interest for both Hong Kong profits tax and salaries tax, when the fund is certified by the Hong Kong Monetary Authority (HKMA).

In this article we will mainly walk you through the basic features of an LPF and an OFC, and outline how the fund manager and the fund can take advantage of the above tax relief.

Common fund structures in Hong Kong

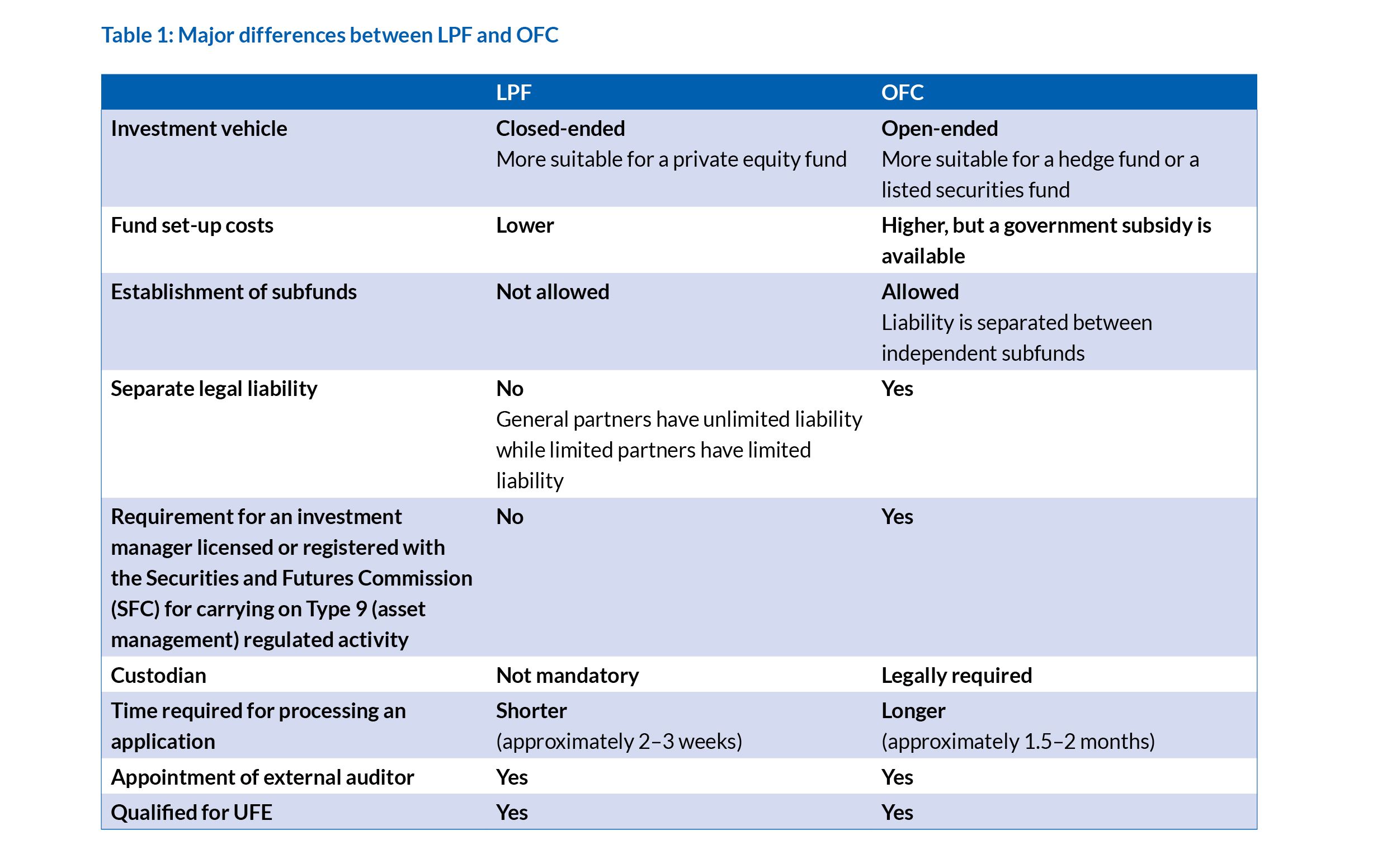

Below, we look at the different features an LPF and an OFC. For a snapshot of the major differences between the two types of fund, see Table 1.

LPF

In the hopes of attracting private investment funds to set up and register in Hong Kong, and ultimately facilitating the channelling of capital into corporates in the Greater Bay Area, the LPF regime was established in August 2020. This is a fund structured in the form of a limited partnership, which will be used for the purpose of managing investments for the benefit of its investors. A fund qualifying for registration under the LPF regime must be constituted by one general partner who has unlimited liability in respect of the debts and liabilities of the fund, and at least one limited partner with limited liability.

OFC

An OFC is an open-ended collective investment scheme that was commonly adopted in July 2018. Structured in corporate form with limited liability and variable share capital, an OFC mainly serves as an investment fund vehicle and manages investments for the benefit of its shareholders. OFCs are therefore not designed to engage in activities such as the commercial trade and business undertaken by conventional companies that are incorporated under the Companies Ordinance (Cap 622).

Attractive government subsidy for OFCs

The features of an OFC are similar to those of the segregated portfolio company as used in the Cayman Islands. In order to enhance the competitiveness of the OFC, an attractive subsidy is now offered to fund managers for the set-up of OFCs or for the re-domiciling of offshore funds to Hong Kong. The subsidy offers a rebate of 70% on all professional expenses that are paid to Hong Kong–based service providers (for example, legal fees for the preparation of incorporation, including any fees incurred in drafting legal documents or offering documents). The tax rebate is subject to a cap of HK$1 million per OFC. Each investment manager can claim a subsidy on a maximum of three OFCs.

It is worthwhile noting that the tax advice in relation to the set-up of an OFC or the re-domiciling of foreign funds are also eligible for the 70% rebate. Investment managers are encouraged to study carefully the Hong Kong tax implications (including but not limited to the availability of the UFE and carried income tax concessions, as well as the traditional capital gains claim). A review of the fund’s private placement memorandum is also often important, as it is a public document providing a significant amount of information on the investment strategy of the fund.

UFE regime

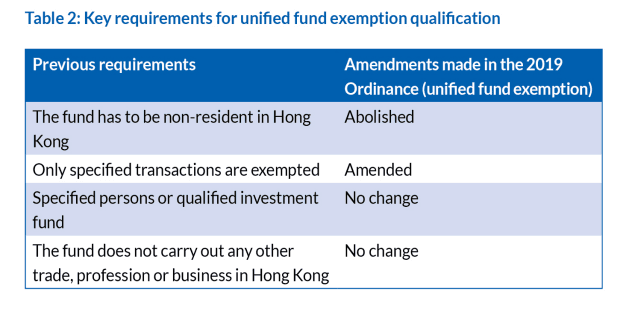

The IRD’s Departmental Interpretation and Practice Note (DIPN) 61 published in June 2020 provided clarification on its view on the UFE regime for both Hong Kong and non–Hong Kong domiciled funds. For more details, please refer to our article – Offshore fund exemption regime for Hong Kong–domiciled funds – published in the August 2020 edition of this journal.

A summary of the key requirements for qualification under the UFE regime is provided in Table 2.

It is worth noting that Hong Kong–domiciled funds are now also eligible to enjoy the UFE, as the non-resident requirement has been abolished. Also, there is no requirement for the directors of the fund to carry out business activities outside Hong Kong.

Specified transactions

Specified transactions include, amongst others, transactions in public securities, private company shares, futures contracts and foreign currencies. Further clarification is required on whether transactions in cryptocurrencies and other virtual assets are specified transactions.

For transactions in private companies, it is common practice for a fund to set up one or more special purpose entities (SPEs) to hold the investments in the investee private company.

SPEs. An SPE must be established for the sole purpose of holding and administering a private company and is not allowed to carry out any other trade or activity after incorporation.

Private companies. While a fund exemption has been extended to private equity funds, additional requirements are imposed on the portfolio company. First and foremost is the 10% threshold imposed on investment in Hong Kong immovable property, whereby the aggregate market value of the holding of immovable properties in Hong Kong cannot account for more than 10% of the total asset value of the respective company.

In addition to the immovable property test, one of the following additional requirements has to be satisfied:

• the holding period test: the fund has to hold the private company for at least two years

• the control test: the fund does not have a controlling shareholding of the private company, or

• the short-term asset test: no more than 50% of the market value of the assets of the private companies are short-term assets (that is, the holding period of the relevant assets is less than three years).

Anti–round tripping provisions

Even when a fund qualifies under the UFE, a deemed taxable income will be imposed on Hong Kong investors of the fund on the exempted assessable profits under the following situations:

• if the Hong Kong investors jointly hold 30% or more of the beneficial interest in the fund, or

• if Hong Kong investors who are associated with the fund hold any beneficial interest in the fund.

Carried interest tax concessions

Under the Inland Revenue (Amendment) (Tax Concessions for Carried Interest) Ordinance 2021, which took effect in May 2021, eligible carried interest arising from in-scope transactions received by qualifying recipients for the provision of investment management services to qualifying payers is exempt from tax in Hong Kong. Tax concessions are available for eligible carried interest received or accrued on or after 1 April 2020.

To distinguish from annual asset management fees, a tax concession is only available to profit-related service fees (that is, carried interest). Generally speaking, only profits above the hurdle rate (benchmark) are expected to generate carried interest for the investment managers. Carried interest distributed by the fund management entity to the individual fund manager is also exempt from Hong Kong salaries tax.

Another essential prerequisite is that ‘in-scope transactions’ refers to those of private equity funds that have already been exempt from profits tax under the UFE. More importantly, the private equity fund has to be certified by the HKMA. An external auditor report is required to be included in the application of certification to the HKMA.

On 31 August 2022, the HKMA released its guidelines on the auditor’s report for application for certification of funds. To apply for certification, a fund has to engage a certified public accountant (practising) to prepare an agreed-upon procedures report in accordance with HKSRS 4400 (Revised). A detailed review of the structure and investment activities of the fund is expected in the agreed-upon procedures report.

Last but not least, the fund manager is also required to fulfil the adequacy test in every relevant year of assessment, as set out below:

• average number of full-time qualified employees in Hong Kong: ≥ 2, and

• annual operating expenditure incurred in Hong Kong: ≥ HK$2 million (US$260,000).

Last piece of advice

While the Hong Kong government is dedicated to promoting both the asset management industry in Hong Kong and Hong Kong–domiciled funds, the IRD has expressed concerns about the potential abuse of fund exemptions, especially on short-term trading of Hong Kong immovable properties.

It is therefore important for the fund administrator to pay close attention to all the above requirements, as failure to comply with any one of the requirements, even for a short period of time during the year, may render the fund ineligible to enjoy the exemption benefits. In order to enjoy the 70% rebate on professional fees for an OFC, you are encouraged to turn to your tax advisor at the initial set-up stage of the fund.