Articles

What you need to know before applying for a certificate of resident status in Hong Kong

Given Hong Kong’s increasing network of Double Taxation Agreements/Arrangement (DTAs), obtaining a Certificate of Resident Status (CoR) in Hong Kong in order to utilise the tax benefits under a DTA has become an important part of tax planning for multinational corporations and Chinese enterprises. Meanwhile, the Inland Revenue Department (IRD) of The Government of the HKSAR is taking a stricter approach when reviewing CoR applications. As such, it is important to understand the definition of a Hong Kong tax resident and the prevailing practice of the IRD before making a CoR application.

Definition of a Hong Kong tax resident

Several years ago, following the definitions stated in the DTA entered into by Hong Kong, being a Hong Kong incorporated company was sufficient to qualify as a Hong Kong tax resident. As such, it was not difficult for a Hong Kong corporation to obtain a CoR.

However, in recent years – as many of you may be aware – following the international practice of avoiding treaty abuse and treaty shopping, the IRD now expects a corporation to build up substance in Hong Kong in order to qualify as a Hong Kong tax resident. In other words, a shell company without substance in Hong Kong is likely to be rejected by the IRD when making a CoR application.

The ‘Departmental Interpretation and Practice Notes No 43 (Revised)’ (DIPN 43) provides some of the IRD’s latest views. In order to be a Hong Kong tax resident, a corporation has to be centrally managed and controlled in Hong Kong. Under DIPN 43, the IRD does not specify the exact amount of substance required, but will look at all facts regarding the management and operations of the applicant company in order to make a decision. It has also explicitly stated that the place of incorporation is not itself conclusive proof of where the central management and control is exercised.

Tax benefits under a DTA

Before we go into the detailed requirements of a CoR application, it would be fruitful to first examine the scenarios under which a CoR would be beneficial to a corporation. A Hong Kong tax resident would be better off if the tax liabilities stated in the DTA were less than that stated in domestic law. As at 30 September 2019, Hong Kong had entered into Comprehensive DTAs with 42 tax jurisdictions, including Japan, the United Kingdom and Indonesia. Please refer to the IRD’s website for the full list of Hong Kong tax treaty partners.

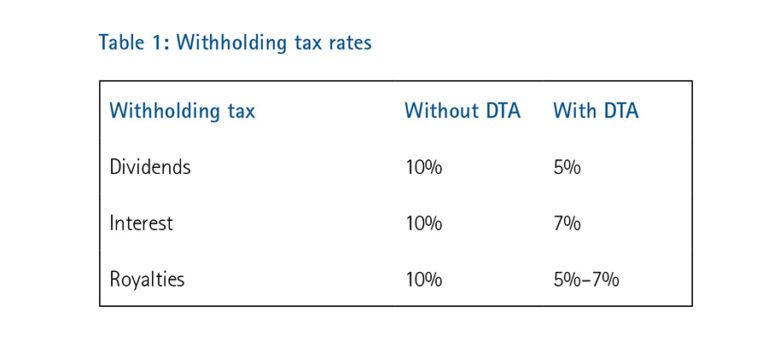

Having said that, the most common DTA applicable to a Hong Kong corporation must be that between Hong Kong and the mainland of China (the Mainland). Table 1 summarises the differences in withholding tax rates on dividends, interest and royalty payments made by Mainland corporations to Hong Kong corporations, with and without the DTA.

These figures partly explain the reason why multinational corporations opt to set up a Hong Kong holding company to invest in the Mainland. If a Hong Kong holding company qualifies as a Hong Kong tax resident and fulfils the Beneficial Ownership requirement under the Mainland’s Public Notice [2018] No 9, it is highly likely that the Hong Kong holding company can enjoy a preferential tax rate of 5% on dividends received from its Mainland subsidiaries.

The preferential tax rate also applies to Mainland enterprises listing on the Hong Kong Stock Exchange. In the common red chip structure, a Hong Kong company would be set up to hold shares of Mainland operating entities. One of the main purposes for setting up a Hong Kong holding company is to reduce the withholding tax rate from 10% to 5% for profit repatriation from the Mainland to Hong Kong. The 5% withholding tax reduction would have a significant impact on the final amount of dividends receivable by investors.

On the other hand, Hong Kong corporations licensing its trademarks, licences or other intellectual properties to Mainland corporations can also enjoy a reduced withholding tax rate if it qualifies as a Hong Kong tax resident.

Other taxation benefits made possible through obtaining CoR status are the elimination of double taxation and a more favourable definition of permanent establishment in the DTA.

Practical experience sharing

As mentioned above, the IRD will look at the place in which the central management and control of a corporation is exercised in order to determine whether a corporation is a Hong Kong tax resident or not. Based on our experience, the IRD will look at the following aspects when reviewing a CoR application:

• whether the directors of the corporation are based in Hong Kong

• whether the board of directors’ meetings of the corporation are held in Hong Kong (that is, physical location of the directors

at the time of the meeting will be taken into consideration)

• whether the corporation maintains an office and/or any other business establishment in Hong Kong

• whether the staff (particularly senior management personnel) of the corporation are based in Hong Kong, and

• whether the profits of the corporation are subject to Hong Kong profits tax.

As the IRD will consider all facts relevant to the management and control of the corporation as a whole, the above list is not intended to be exclusive and at the same time a corporation may not have to fulfil all of the above requirements to qualify as a Hong Kong tax resident. For each of the above factors, the IRD will first examine whether the corporation has built up the relevant substance in Hong Kong, and will then compare the substance built up by the corporation in Hong Kong and other tax jurisdictions.

Administrative procedures

Applications for a CoR are made on a calendar year basis, regardless of the accounting year-end date of the applicant. If the applicant would like to obtain the tax benefits under two separate DTAs, two separate applications have to be made, despite the fact that the requirements will be more or less the same. Application forms IR1313A (applicable to the DTA between Hong Kong and the Mainland) and IR1313B (applicable to all other DTAs entered into by Hong Kong) should be filled in and submitted to the IRD.

A CoR is generally valid for one year. To ease the administrative burden, a CoR in respect of the DTA between Hong Kong and the Mainland is generally valid for three years, provided that the operations of the Hong Kong company remain substantially unchanged.

It takes around 21 business days for the IRD to process a CoR application. Should the IRD consider that it needs additional information and supporting documents to make a decision, it will issue an enquiry letter to the applicant. At that stage, the IRD does not provide a specific timeframe for reviewing the applicant’s reply to the enquiry letter.

In view of the above, it is advised that:

• sufficient information and supporting documents should be submitted to the IRD with the initial application in order to avoid any

delay in the application process, and

• as the CoR for the DTA between Hong Kong and the Mainland is valid for three years, an application for a new CoR could be

submitted well in advance, to allow a sufficient buffer time in the application process.

Last piece of advice

Based on our experience, a failed application renders it more difficult for a corporation to successfully obtain a CoR in the future, while a successful application tends to make future applications easier.

As such, we encourage corporations to look for tax advisors to examine whether the current status of the corporation would qualify it as a Hong Kong tax resident or not. If insufficient substance is maintained in Hong Kong, to enhance the chance of success, tax planning should be carried out before submitting a CoR application to the IRD.

The clarity and depth of information provided in the article on CoRs in Hong Kong really helped our company navigate the complex tax landscape. Thanks to the detailed guidelines, we were able to prepare our application thoroughly and achieved a successful outcome. Highly recommend this resource for anyone dealing with corporate taxes in Hong Kong.

I found the detailed breakdown of the CoR application process and requirements extremely useful. It enabled our company to prepare adequately and avoid potential pitfalls that could have delayed our application. This guidance was instrumental in our successful CoR acquisition.