Articles

IRD's New Letter Signals Major Tax Shake-Up for Multinationals in Hong Kong Under BEPS 2.0

IRD's New Letter Signals Major Tax Shake-Up for Multinationals in Hong Kong Under BEPS 2.0

.

January 2026 | ONC LAWYERS

1. IRD Issues Formal Notification on GloBE Rules – What It Means for Your Business

.

If you're part of a multinational enterprise (MNE) operating in Hong Kong, brace yourself: In September 2025, the Inland Revenue Department (IRD) dropped a bombshell letter directly to affected companies, confirming the immediate rollout of the Global Anti-Base Erosion (GloBE) Rules and the Hong Kong Minimum Top-up Tax (HKMTT). This isn't just routine paperwork – it's a game-changer that could hit your bottom line hard if your effective tax rate dips below 15%.

This letter, issued under the OECD's BEPS 2.0 Pillar Two framework, targets large MNE groups with annual consolidated revenues over EUR750 million. It demands compliance starting now, forcing companies to reassess their tax strategies or face top-up taxes collected right here in Hong Kong. Ignore it, and you risk not only penalties but also foreign governments swooping in to claim what's owed. Hong Kong's move protects its own taxing rights, but for MNEs, it spells urgency: higher taxes, heavier reporting, and potential restructuring to avoid the fallout.

This notification underscores Hong Kong's shift from its traditionally business-friendly, low-tax haven status to a stricter regime aligned with global standards. It's a wake-up call – transparency and fairness are in, unchecked profit shifting is out. If your group qualifies, this letter isn't optional reading; it's a mandate that could reshape your operations overnight.

.

2. Decoding the IRD Letter: GloBE Rules and HKMTT Explained

.

At the heart of the IRD's letter is Hong Kong's adoption of the GloBE Rules, a global mechanism to slap a 15% minimum effective tax rate (ETR) on qualifying MNEs in every jurisdiction. If your ETR falls short in Hong Kong, the HKMTT kicks in as a domestic top-up tax, ensuring the IRD collects the difference locally – before any overseas authority can.

Key highlights straight from the letter:

• Effective Date: Hits fiscal years starting on or after 1 January 2025 – no grace period.

• Who It Targets: MNE groups with over EUR750 million in consolidated revenues in at least two of the last four years.

• Why It Matters: Hong Kong's 16.5% profits tax rate has long been a draw, but BEPS 2.0 changes that. Low-ETR strategies could now trigger immediate top-ups, eroding competitive edges and boosting tax bills.

• Legal Backbone: Backed by the Inland Revenue (Amendment) (Taxation on Specified Foreign-sourced Income and Other Measures) Ordinance 2024.

The letter makes it crystal clear: This isn't about voluntary alignment; it's enforced compliance to prevent profit erosion and maintain Hong Kong's global standing. For MNEs, it means potential tax hikes and a scramble to adapt, all while preserving Hong Kong's role as a regional hub.

3. Who Gets Hit? Entities and Thresholds Spotlighted in the IRD Notification

The IRD letter doesn't mince words: If your MNE group crosses the EUR750 million revenue threshold, every Constituent Entity in Hong Kong – from parents and subsidiaries to permanent establishments and joint ventures – is in scope.

The IIR (please refer to footnote for detailed definition) mandates that the ultimate parent entity of an MNE group pay a top-up tax if the effective tax rate in any jurisdiction where the group operates is below the global minimum rate of 15%. This rule essentially ensures that profits are taxed at a minimum rate regardless of where they are earned.

Critical details from the letter:

• Constituent Entities: All group members subject to GloBE, with exemptions only for governments, international orgs, and select investment funds.

• Threshold Check: Based on consolidated revenues – if you qualify, the letter requires immediate disclosure of your group structure, fiscal year-end, and Ultimate Parent Entity (UPE).

This broad net could ensnare more companies than expected, leading to unexpected tax exposures. The IRD's emphasis on OECD alignment means no loopholes: Non-compliance risks audits, penalties, and even double taxation if foreign rules apply first.

4. How the Letter's Rules Crunch Numbers: ETR Calculations and Top-Up Taxes

The IRD letter lays out the math in stark terms: Calculate your jurisdictional ETR by dividing adjusted covered taxes by GloBE income. Below 15%? Prepare to pay up via the HKMTT.

A chilling example from the framework:

• Your ETR: 10%

• Minimum Required: 15%

• Top-Up Hit: 5% on GloBE income – collected by the IRD to keep it local, not leaked abroad via Income Inclusion Rule (IIR) or Undertaxed Payments Rule (UTPR).

This could mean millions in additional taxes for under-taxed entities. The letter stresses efficiency and certainty, but the reality? MNEs face immediate pressure to boost ETRs through restructuring or losing incentives, all to avoid the IRD's grasp.

5. Safe Harbour Rules

To soften the blow, the IRD letter incorporates OECD's Transitional Safe Harbours for 2024-2026, offering short term relief – but only if you qualify.

Relief options highlighted:

• Simplified ETR Test: Skip top-ups if your rate already tops 15% (rising thresholds up to 17% ahead).

• Routine Profits Test: Tiny profit in a particular tax jurisdictions is exempt.

• De Minimis Test: Total GloBE income is less than €10 million and Profit before taxation is less than €1 million

These are band-aids, not cures. The letter warns: Use this time to overhaul systems, or face full-force compliance post-2026. Delaying could amplify risks when the safety nets vanish.

6. The Letter's Demands: Reporting Deadlines and Penalties

.

Must-dos:

• What to Submit: Full entity breakdowns, revenue splits, ETR calcs, and top-up details.

• Deadline: 15 months post-fiscal year (18 for year one) via eTAX.

• Consequences: Fines, prosecutions under the Inland Revenue Ordinance for slip-ups.

This ramps up costs for data systems and cross-team coordination. The letter's tone? Compliance isn't optional – missteps could trigger IRD scrutiny and erode trust.

7. Real-World Shocks: How the IRD Letter Impacts MNE Operations

The IRD's notification isn't abstract; it's a direct threat to status quo:

• Tax Strategies Upended: Offshore exemptions? Preferential rates? They might not shield you anymore – model exposures now or pay later.

• Tech Overhaul Required: Integrate global data for accurate reporting; lag behind, and errors compound.

• Group-Wide Panic: Coordinate across borders to align on ETRs and filings – silos could cost dearly.

• Risk Management Crunch: Document everything; weak governance invites audits and reputational hits.

For Hong Kong-based MNEs, this letter could force relocations, mergers, or tax hikes – a stark reminder that the low-tax era is evolving fast.

8. Final Warning: Navigate the IRD Letter or Risk the Storm

.

The IRD's September 2025 letter on BEPS 2.0's GloBE Rules and HKMTT isn't just policy – it's a seismic shift demanding action. Hong Kong is fortifying its tax sovereignty while embracing global norms, but for MNEs, it means higher stakes, tighter scrutiny, and potential financial pain.

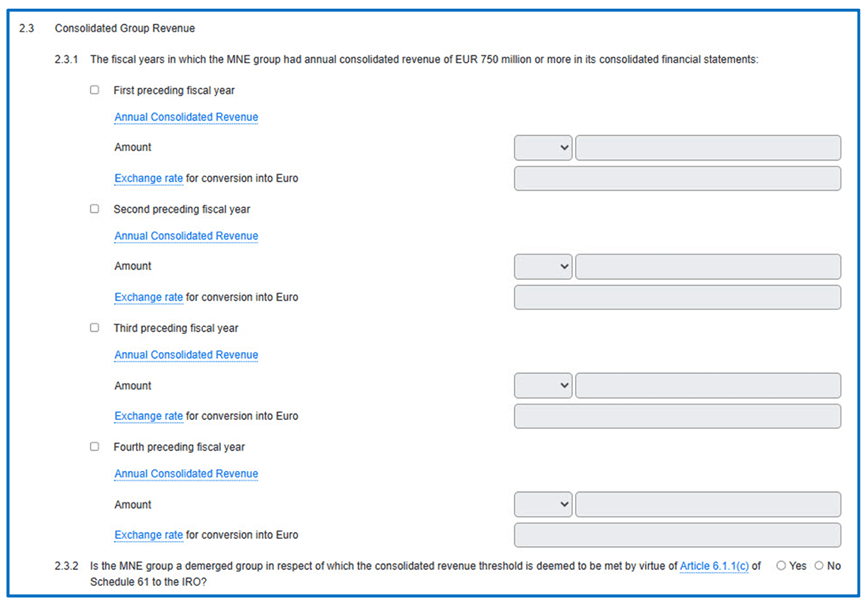

The image below is an excerpt from the Top-up Tax Notification form. It illustrates that the consolidated revenue for each year must be reported accurately, failure to do so will result in the system rejecting the submission. BEPS 2.0 is already an inevitable challenge that MNEs must address.

.

.